The Canadian banking landscape is undergoing a transformation. In this article, we’ll delve into the fundamentals of mortgages in Canada and examine the composition of the market in terms of borrowers. Stay tuned to discover how these shifts are set to reshape homeownership in Canada.

How Many Banks Are in Canada?

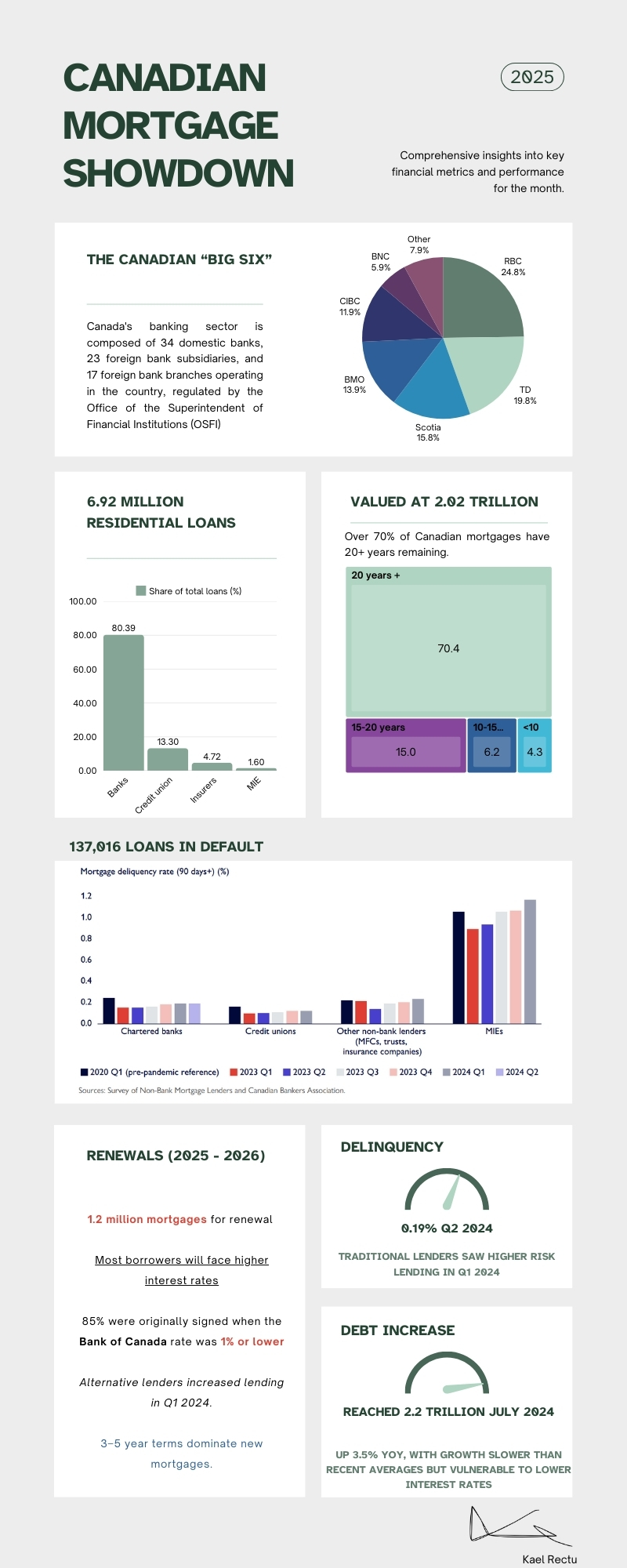

Canada’s banking sector is composed of a mix of domestic banks, foreign bank subsidiaries, and credit unions. As of 2024, there are 34 domestic banks, 23 foreign bank subsidiaries, and 17 foreign bank branches operating in the country, regulated by the Office of the Superintendent of Financial Institutions (OSFI). The industry is dominated by the “Big Six”

Market Share

The Big Six banks collectively hold approximately 90% of the market share in Canada’s banking sector. Here is a rough breakdown of their market share as of recent estimates:

Check out our bank comparison article or dive into an analysis of banking disputes to find out which canadian bank files the most lawsuits.

The Mortgages Landscape in Canada

So, how many mortgages are we talking about here?

Canada’s residential mortgage market is vast, with approximately 6.92 million residential mortgage loans nationwide. These loans account for a staggering total value of $2.02 trillion. Of this, 2.15 million mortgages, representing $558.42 billion, are insured through the Canada Mortgage and Housing Corporation (CMHC), reflecting the critical role of mortgage insurance in safeguarding lenders and borrowers alike.

Banks continue to dominate the mortgage landscape, holding 80.39% of the market, followed by credit unions at 13.30%. However, credit unions face the highest default rates and challenges with unsecured loans.

Using realistic estimates based on market dynamics and available financial reports, here’s a possible breakdown of the 6.92 million residential mortgages among Canada’s “Big Six” banks:

| Bank | Mortgages |

|---|---|

| RBC | ~1,522,400 |

| TD | ~1,245,600 |

| Scotia | ~1,038,000 |

| BMO | ~899,600 |

| CIBC | ~830,400 |

| BNC | ~415,200 |

The estimated breakdown of residential mortgages among Canada’s “Big Six” banks is based on their relative market share, as derived from publicly available financial statements and industry reports. Market share percentages were assigned to each bank considering their reported mortgage portfolios and overall dominance in the mortgage market. The total number of residential mortgages in Canada, 6.92 million, was then distributed proportionally according to these market share estimates. Larger banks like RBC, TD, and Scotiabank were allocated higher shares due to their leading positions in the industry, while BMO, CIBC, and National Bank of Canada received smaller, though still significant, portions reflecting their respective contributions to the mortgage landscape. These calculations provide a realistic approximation of how the Big Six manage the majority of residential mortgages in Canada.

And they are not anywhere near from being paid.

Over 70% of Canadian mortgages have a remaining amortization period of 20 years or more, while 15% fall within the 15-20 year range. Recent legislation has further extended the maximum allowable amortization to 30 years, giving borrowers more flexibility but also extending the financial commitment significantly.

The Canadian mortgage market is significant, with millions of active mortgages spanning both consumer and commercial sectors. For the consumer segment alone, the market is valued at $2.02 trillion, which represents approximately 75% of Canada’s GDP. This highlights the critical role mortgages play in the nation’s economy and financial stability.

As of Q2 2024, 137,016 loans are in default, marking an increase from the previous year. The overall mortgage delinquency rate rose to 0.19%, reflecting growing financial pressures on borrowers. Traditional lenders experienced a higher risk of 0.19% delinquency in Q1 2024, but the trend stabilized slightly in subsequent quarters. These figures underscore the ongoing challenges in managing household debt amidst a shifting economic landscape.

- Commercial Mortgages: Over 500,000 active commercial mortgages.

- Unique Mortgage Holders: Around 5.5 million Canadians hold at least one mortgage.

- International Mortgages: Some Canadian banks offer mortgages to international buyers, though these represent a small fraction of the total market.

Current Types of Mortgages in Canada

Canadian borrowers have access to several types of mortgages to suit different financial needs. The primary mortgage types include:

- Fixed-Rate Mortgages: The most popular option, offering stability with fixed interest rates for terms ranging from 1 to 10 years.

- Variable-Rate Mortgages: Interest rates fluctuate with the prime rate, often leading to lower costs in a declining rate environment.

- Hybrid Mortgages: A mix of fixed and variable components, offering flexibility.

- Open Mortgages: Allow prepayments without penalties, ideal for borrowers expecting to pay off their mortgage quickly.

- Closed Mortgages: Lower interest rates but with restrictions on prepayments.

- Reverse Mortgages: Available to seniors, allowing them to access home equity without monthly payments.

Stay tuned for our 2025 Mortgage Insights: Trends and Reviews.

Conclusion

The Canadian mortgage market is a cornerstone of the nation’s financial landscape, deeply intertwined with the economy and the lives of millions of Canadians. With $2.02 trillion in residential mortgage loans, representing 75% of the country’s GDP, the sheer scale and significance of this sector cannot be overstated. While the market offers flexibility with a variety of mortgage types to suit different needs, challenges such as rising delinquency rates and extended amortization periods highlight the importance of sound financial planning.

As borrowers navigate longer mortgage commitments and lenders adapt to evolving risks, the sector continues to evolve, driven by regulatory changes, market dynamics, and consumer demands. The dominance of banks, rising prominence of alternative lenders, and increasing attention on sustainability reflect a market in flux. Ultimately, the Canadian mortgage industry’s resilience and adaptability will shape its ability to meet the needs of future generations, sustaining its critical role in fostering homeownership and economic stability.

Kael Rectu

Sources

CMHC: Residential Mortgage Industry Data Dashboard

Bank of Canada: Financial System Review 2024

Statistics Canada: Canadian Housing Statistics Program

0 responses to “The 2025 Canadian Mortgage Showdown”